Key points:

- Mortgage rates nearly tripled between late 2020 and late 2023.

- Still, rates are nowhere near the highs homebuyers saw in the early 1980s.

- When it comes to mortgage rates, “high” is a matter of perspective — prospective buyers need to figure out what’s important to them in order to time their loan well.

On the one hand, mortgage rates are significantly higher than they were a few years ago. On the other, they’re nowhere near historic highs. That means there’s no clear-cut answer to the question: are mortgage rates high right now? Homebuyers need to decide what high means to them, and what the right time to get a loan looks like for their specific situation.

Are mortgage rates high right now? If you’ve been thinking about buying a house, that was probably one of the first questions that came to mind.

Maybe you’re a first-time homebuyer and this is your opening foray into the world of mortgage interest rates. Maybe you bought your home a while ago but you’re considering a refinance or a move. Whatever the case may be, comparatively low interest rates make it more appealing to make moves.

So, where are we at currently? Are mortgage rates high right now? The answer is yes. And the answer is also no. Let’s dig in to help you understand how both can be true — and what it means for your homebuying or refinancing journey.

Yes, mortgage rates are high right now

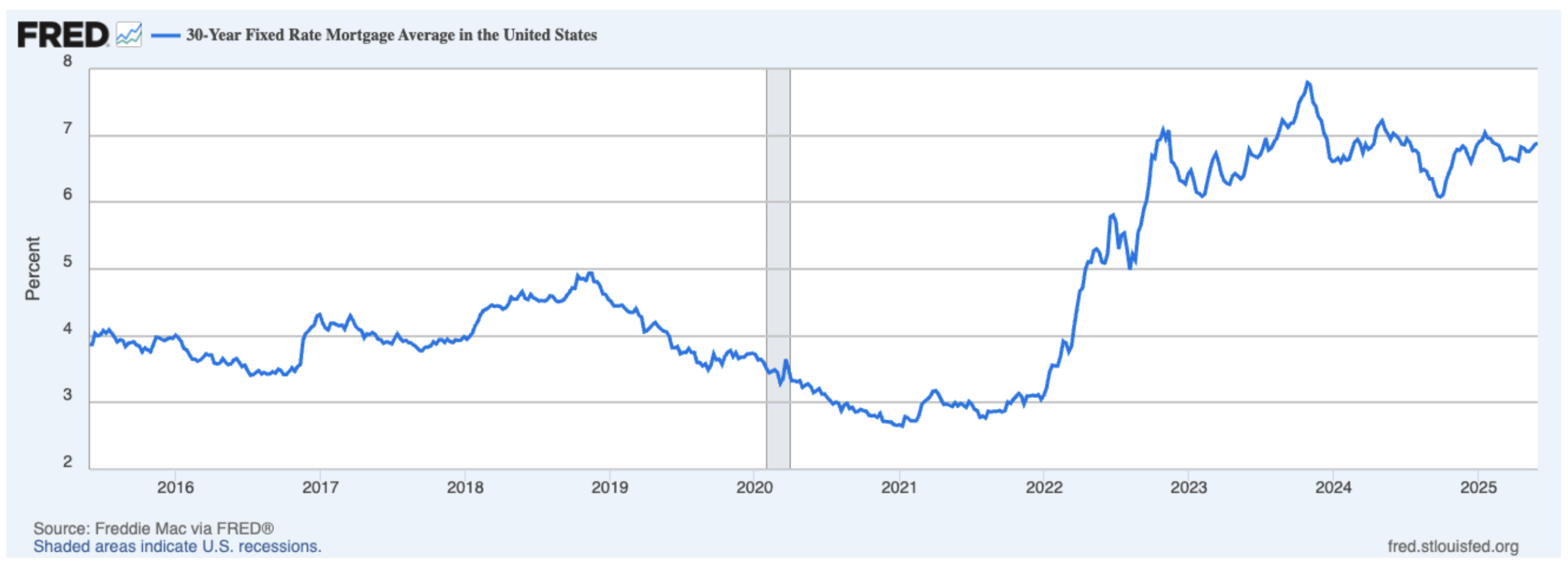

If you look at mortgage rates over the last decade, today’s average of just under 7% doesn’t look overly favorable. While sub-7% rates are certainly better than many homebuyers landed a couple of years ago, they can’t hold a candle to the historic lows we saw in the early 2020s.

Starting in late 2018, rates began a somewhat steady slide. By late 2020, the average rate for a 30-year fixed-rate mortgage was around 2.66%, per Federal Reserve Economic Data (FRED).

Unsurprisingly, that led to a massive mortgage boom, both in mortgages for new home purchases and in refinances.

Coming out of the pandemic, though, rates hiked up. So, are mortgage rates high right now? If you compare today’s rates against the rates we saw in 2020 and 2021, absolutely.

That doesn’t necessarily mean you should wait to buy or refinance, though. Rates might look high when you evaluate the short-term trends. Zooming out, though, paints a different picture.

No, mortgage rates aren’t high

While ten years might seem like a long time — and plenty to evaluate mortgage rate trends — most mortgages last a lot longer than a decade. In fact, the majority of homebuyers go with a 30-year loan. It makes sense, then, to look at rates over a longer span. The below graph from FRED shows how today’s rates stack up against rates spanning all the way back to the 1970s.

With that perspective, you come up with a different answer when asking, “Are mortgage rates high right now?” While they might feel high compared to the historic lows of five years ago, rates are lower now than they were in the 70s, 80s, and much of the 90s. They’re nearly triple the low point of 2020, but they’re just over a third of the 18.63% the average homebuyer paid in interest in October 1981.

To add a little more context here, someone who got a 30-year mortgage in 1995 and is just now paying it off probably paid a comparable rate to what homebuyers are seeing right now.

Timing homebuying to get the best mortgage rate is tricky business

To make homebuying as affordable as possible, you want to get the best mortgage interest rate you can. That’s led to a lot of folks waiting for rates to come down.

Unfortunately, they’ve been holding that bated breath for a while now.

People have been speculating that the Federal Reserve would cut its federal funds rate for some time. Mortgage rates aren’t directly tied to the Fed’s rate. But a rate slash from Jerome Powell’s team usually moves the needle downward on a range of interest rates, including mortgage rates. To date, though, the Fed hasn’t cut rates in all of 2025.

All told, there are a lot of economic and even geopolitical factors that impact mortgage rate movement. The vast majority of them are out of your hands. While you wait for rates to come down, your dream home might get snapped up by another buyer.

The question, then, shouldn’t be: “Are mortgage rates high right now?” Instead, it should be, “Can I get a rate that makes it a good time for me to buy?”

Deciding on the right time to buy or refinance

A lot of the things that affect mortgage rates are out of your control. But the power is in your hands in one area: timing. Identifying the right time to get a new mortgage — whether that means buying a house or refinancing into a new loan — means evaluating not just rate trends but also factors that are specific to you. Specifically, look at:

Your long-term goals

What does homebuying or refinancing achieve for you? Does it offer stability? Wealth-building? The clout of homeownership? Your answers are probably different depending on whether you’re buying a new house or refinancing into a new loan.

Buying

If you want to buy, think carefully about what this major purchase will mean for your life long-term. There’s a general rule that says you should stay in a house for at least five years before selling. This gives you enough time to recoup your closing costs and build some equity, making the purchase a financial savvy move.

Think, then, about what your life will look like in five years. Will you still want to be in the same neighborhood? If you’re happy with your job or you love your community of friends, that answer might be easy. But if you could see yourself making some major changes in the near future, it might not be a good time to buy — regardless of what mortgage interest rates are doing

Refinancing

Experts recommend refinancing when you can get a lower interest rate. With the way rates have moved in the last 25 years, averages today are higher than they were when most homebuyers got their loans.

That doesn’t mean you should rule out refinancing, though. If you have a long-term goal of being debt-free sooner and you can afford bigger monthly payments, for example, it might make sense to refinance from a 30-year loan to a 15-year one. As an added bonus, lenders usually offer lower rates for shorter mortgages, so you might be able to qualify for a better rate with this option.

Refinancing also might work for your situation if you’re considering a cash-out refi. Even with rates somewhat high today, being able to liquidate some of your equity in your house can move you toward other goals. If you need money for education, a new business venture, or to pay off other higher-interest debt, this option might make sense.

Your current financial situation

Mortgage rate movement is just one piece of figuring out how much your home loan will cost you in interest. That’s because, up to this point, we’ve been talking about average interest rates. But there’s no guarantee you’ll qualify for the average.

If you have an excellent credit score, a solid amount in savings, and a steady job, you might be able to beat out the average. If your financial profile is less-than-stellar, though, you need to be ready to pay more in interest.

Lenders will evaluate things like your bank statements and pay stubs to decide how risky you look to them. They’re willing to take on more risk provided you’re willing to pay a higher interest rate.

Ask yourself, then, “Are mortgage rates high right now — for me in particular?” In other words, are you in good financial standing to get the most competitive rate?

If your credit score could use some work or you don’t have steady employment, you’re not guaranteed a good rate even in a low rate environment. If you’re thinking about waiting for rates to come down anyway, use the time to put some work into looking as appealing to lenders as possible.

Keeping a finger on the pulse of mortgage rates

You shouldn’t have to guess at where rates are and how they’re moving. To get a steady feel for what’s going on with mortgage interest rates, bookmark our rate tables. Checking in regularly means you can watch as trends emerge — and better pinpoint the right time to buy or refinance.