Key points:

- Data shows that the interest rates quoted by different lenders often vary by about 0.5%.

- That seemingly small difference can translate to thousands of dollars in potential savings each year.

- Over a 30-year mortgage, an interest rate that’s 0.5% lower can save the homeowner tens of thousands.

Mortgage rates vary from lender to lender, even for the same type of loan with the same balance and the same repayment timetable. Because of this, mortgage rate shopping helps borrowers identify the best rate for them. Data shows that this effort can save them thousands of dollars a year — and a serious sum of money over the life of the loan.

If you’re car shopping, you probably aren’t going to drive a car off the first lot you visit. Whether you look at your options online or physically visit a few different dealerships, you know that shopping around can help you save. And when it comes to something expensive like a vehicle, it’s worth doing your homework.

Houses are a lot pricier than cars, so the act of comparison-shopping gets extra important there. We’re not just talking about comparing the price of different properties, either. Over time, mortgage rate comparison can save you tens of thousands of dollars.

What the data says about mortgage rate differences

Comparing rates from different lenders matters because of something called dispersion. Basically, this is the technical term for varieties in pricing.

Lenders have their own proprietary processes and algorithms for deciding how much interest to charge each individual borrower. As a result, the rate one lender offers you will probably be different from the rate you get quoted from another lender, even for the same loan type, length, and amount.

Data from the Consumer Financial Protection Bureau (CFPB) shows that borrowers see pretty big price dispersion across loan categories. That’s true whether they’re evaluating lenders for a conventional loan, one backed by the Federal Housing Administration (FHA) or Department of Veterans Affairs (VA), or a jumbo loan.

Per that CFPB report, it’s pretty common to see 50 basis points (or 0.5%) between rates quoted by different lenders, even in the same loan categories. As the report points out, “50 basis points yearly is comparable to the Government Sponsored Entities (GSEs) loan-level price adjustment differences between borrowers with credit scores below 620 and borrowers with credit scores above 740.”

You might have put some work into getting ready to apply for a mortgage — but boosting your credit score by 120 points isn’t realistic for most folks. Fortunately, you don’t have to pull off that massive jump. Comparing multiple lenders can help you see comparable savings.

How much mortgage rate comparison can help you save

A 0.5% rate difference doesn’t sound big, but the savings it can deliver absolutely are. Specifically, that can save you:

$50–$100 a month ($600–$1,200 a year)

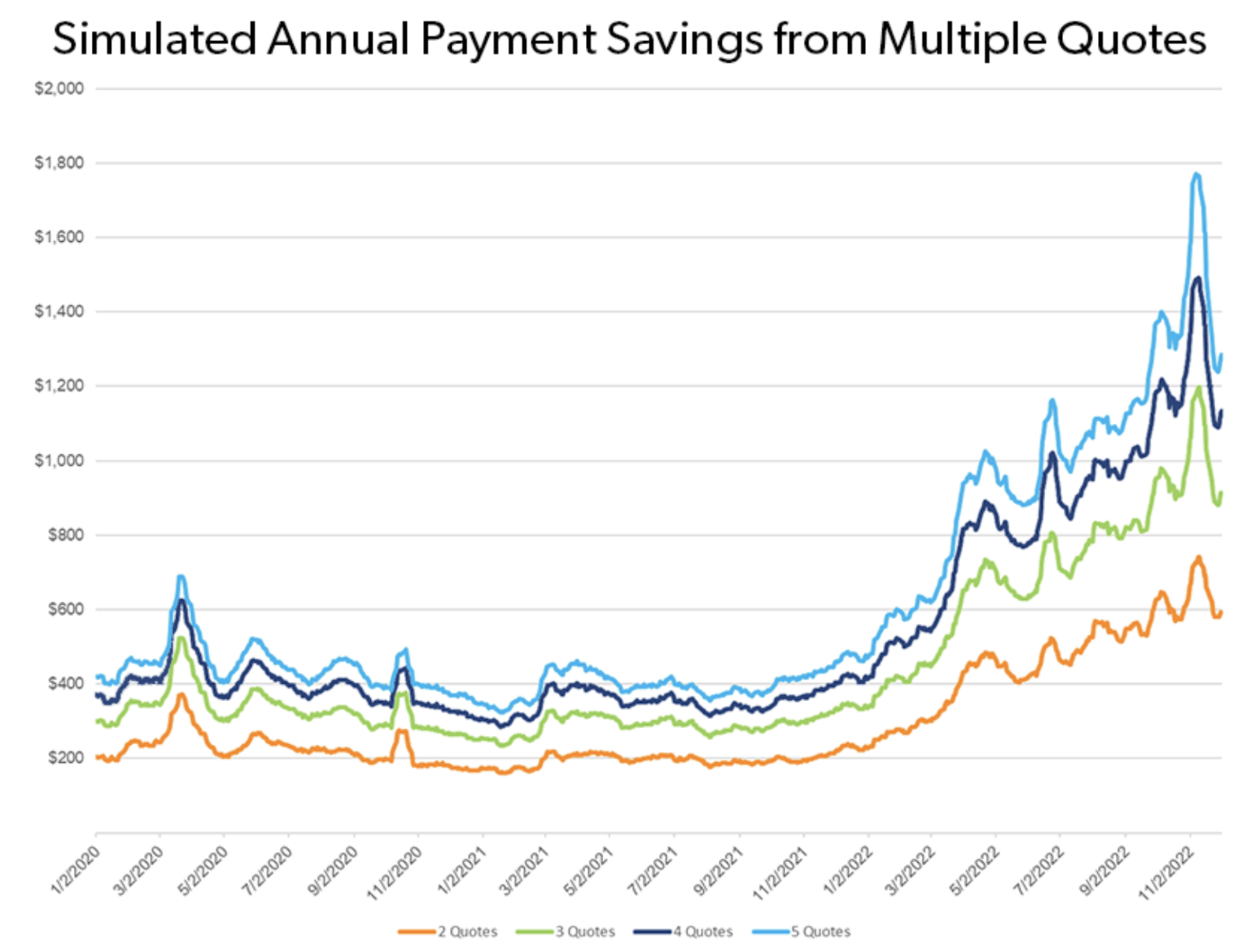

Freddie Mac, a GSE that plays a huge role in the U.S. mortgage market, conducted some research.

The Freddie Mac team found that mortgage rate comparison can save you hundreds if not thousands of dollars per year. In that study, borrowers could have saved as much as $600 a year (that’s $50 a month back in your pocket) just by getting two quotes.

And in the Freddie Mac research, more mortgage rate comparison yielded more money saved. Borrowers who got four or more rate quotes could have saved $1,200 a year, or $100 a month.

If you’re a visual learner, this graph from the Freddie Mac findings can help you get a better feel for the financial benefit of mortgage rate comparison:

$50–$100 a month in savings is already pretty appealing. The real value, though, builds up over time.

Tens of thousands of dollars over a 30-year mortgage

The CFPB has a handy calculator you can use to explore this for yourself. Under the “Explore what a lower interest rate means for your wallet” header, you can compare two different mortgage interest rates to see how much that interest will cost you in five and 30 years. Put the home price and loan term in the right-hand column for more accurate information.

Let’s use that calculator to crunch some numbers. Say you buy a $400,000 house and you put 5% down ($20,000). That leaves you with a starting mortgage balance of $380,000.

Now, let’s imagine you got two interest rates quoted to you: 6.625% and 7.125%.

In the first five years, that lower rate saves you $9,562 in interest. That’s nearly $10,000 you can put toward home improvements, vacations, or anything else you want or need.

If you stay in that house and keep that mortgage for 30 years, that 0.5% lower rate saves you $45,702 overall.

You don’t need to see a half-percentage in difference to see savings, either. Even a slightly lower rate can help you pocket thousands.

Let’s take the same scenario, but compare rates of 6.7% and 6.875%. That’s a rate difference of 0.175%, which might seem too small to make a difference. Actually, though, that can save you $3,345 over five years, and nearly $16,000 over 30 years.

Yes, mortgage rate comparison takes some work. But it can quite literally pay off.

Make sure you’re comparing apples to apples

Mortgage rate comparison yields the best results when you’re comparing the same offering from different lenders. Or, in other words, when you compare apples to apples. If you compare an apple to, say, an orange, you don’t learn much.

That means you want to compare the rates lenders offer for the same kind of loan product with the same basic features (loan amount, repayment term, etc.).

We have a few tips to help there:

- Watch for points on advertised rates: Lenders increasingly feature their lowest current rate on their websites. Theoretically, that makes it easy to see who’s offering the best rate. But be advised: a lot of advertised rates include mortgage points. With points, the borrower hands over a lump sum of money on the frontend to get a lower rate. Usually, one point lowers the rate by 0.25%. If one lender is advertising a 7% interest rate, then, and another is advertising a 6.5% rate with two mortgage points, their starting rates are the same. (6.5 + [2 mortgage points * 0.25] = 7.0)

- Make sure the loan details are the same: Lenders almost always offer lower interest rates for adjustable-rate mortgages than fixed-rate ones. The same is true for shorter loans; a 15-year mortgage usually has a lower rate than a 30-year one. Bigger loan balances and smaller down payments also affect your rate. You won’t know which lender truly offers the lowest rate, then, unless you’re comparing the same kind of loan with the same details. As you work on mortgage rate comparison, check that all of these features are the same:

- Loan type (e.g., conventional, FHA-backed, jumbo)

- Loan term (the amount of time you have to repay)

- Interest rate type (fixed vs. adjustable)

- Loan amount

- Down payment amount

- Compare annual percentage rates (APRs): Interest rates are one thing. APRs tell you how much the loan will cost you including the interest rate and the fees that lender charges. As a result, comparing APRs from different lenders — rather than the interest rate alone — can give you a better idea of which loan is really the best deal.

- Get personalized quotes: The interest rate you’ll get charged depends on some factors that are specific to you, like your credit score, income, and the address of the house you want to buy. Getting a personalized quote means the lender has factored those things in, supporting your mortgage rate comparison efforts.

Getting started with mortgage rate comparison

Comparing rates helps you save money, but it can be overwhelming, especially at the start. So many lenders operate today that narrowing down your options usually feels tricky.

Using a mortgage rate table helps here. This gives you a better idea of what lenders are currently offering so you can decide where to start. Try to identify at least a few lenders from the rate table who feel like a fit to you. Then, get quotes from each to see who can offer you the lowest rate — and, ideally, save you thousands.